Key Takeways

-

The US-China tech rivalry has drastically transformed the global electronics sector since 2017, with both nations using tariffs, export controls, and market access restrictions in their pursuit for technological supremacy. Despite the shift leading to $150 billion in lost exports for China, interdependence persists, as a significant portion of US semiconductor machinery still goes to China.

-

US companies dominate the global electronics landscape, capturing 54% of industry profits, increasing to 88% when factoring in Asian competitors. In contrast, Chinese firms only attain 7% of global profits, indicating a considerable gap in leadership, especially within strategic semiconductor segments.

- The ongoing competition hints at a potential industry shift driven by innovation, as both countries are determined to achieve technological leadership and diminish mutual reliance. This ambition may incite market upheaval, reminiscent of Japan’s past decline in semiconductor supremacy due to evolving technology and US trade strategies.

The US-China tech rivalry has reshaped the global electronics sector, with both countries competing for technological dominance. This article explores the long-term implications of this competition, focusing on trade disruptions, innovation, and future industry trends.

The US–China tech war has intensified dramatically since 2017, employing a full spectrum of measures from tariffs and export controls to restrictions on market access in a race for technological dominance that is reshaping the global electronics landscape. While our calculations indicate a substantial shift in US imports away from China that has cost the latter close to USD150 billion in lost exports since 2017 (Chart 1), they also suggest that underlying, mutual interdependence remains deeply rooted in the very structure of the industry: 29% of US semiconductor manufacturing machinery exports flow to China, and US electronics imports from Mexico, Taiwan and Vietnam incorporate a great deal of Chinese value-added.

US imports of electronic devices by country of origin (%)

Data for the graphs in .xls format

Resilience of US-China Electronics Ties

If the ties connecting the US and Chinese electronics industries have proven more resilient than what headline bilateral trade figures might suggest, it is largely because the US administration’s long-term drive to cut ties with China contradicts the short-term interests of corporate America and the world’s most dominant electronics companies. We estimate that over the last decade US companies alone accounted for 54% of global electronics profits, a share that balloons to 88% when including their Japanese, South Korean, and Taiwanese peers (Chart 2).

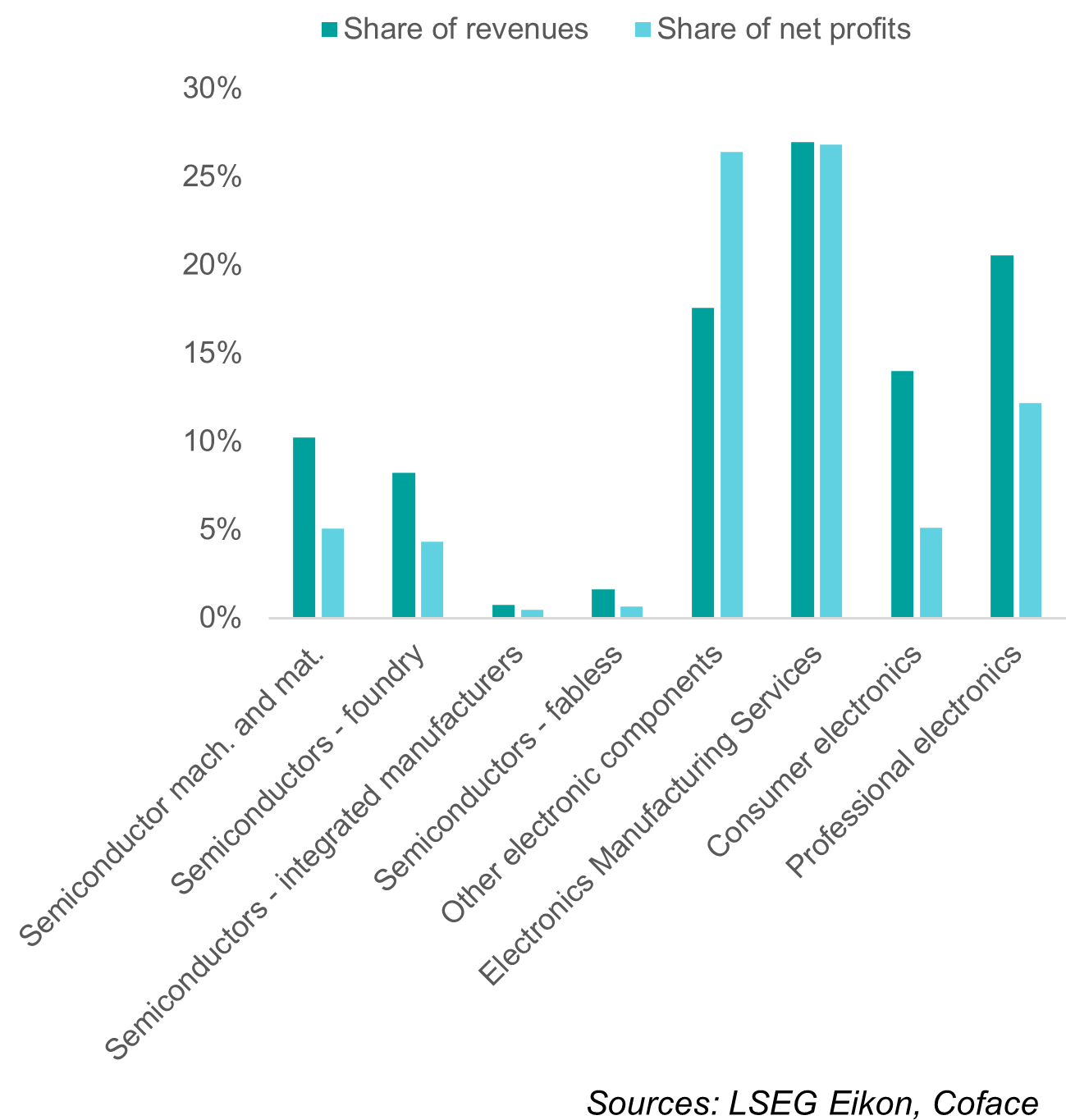

Meanwhile, despite surging sales and remarkable technological progress, Chinese companies only secured 7% of global industry profits and are still lagging far behind leaders in the all-strategic semiconductor segment (Chart 3). A major supplier of critical inputs, an unmatched manufacturing hub and one of the world’s largest consumer markets for electronics, China resembles more a condition for, rather than a threat to, the profitability of dominant US electronics companies.

Share of listed electronics companies in sales and profits by headquarter location in 2014-2023 (%)

Data for the graphs in .xls format

Share of listed Chinese companies in global sales and profits by segment, 2014-2023 average (%)

Data for the graphs in .xls format

However, the assumption that current patterns are going to continue during the coming years is at complete odds with the deep resolve of the US and China to maintain or acquire technological leadership and reduce dependencies, often by using trade as a weapon. Such a belief also discounts the possibility of a major industry shake-up triggered by radical innovation – a feature of the electronics industry. Home to more than 50% of global semiconductor production in the 1980s, Japan’s dominance was undermined by the rise of personal computing and the US’s strategic interventions to limit Japanese exports. Similarly, the smartphone…